Agent of the Wild

November Real Estate Newsletter 2025

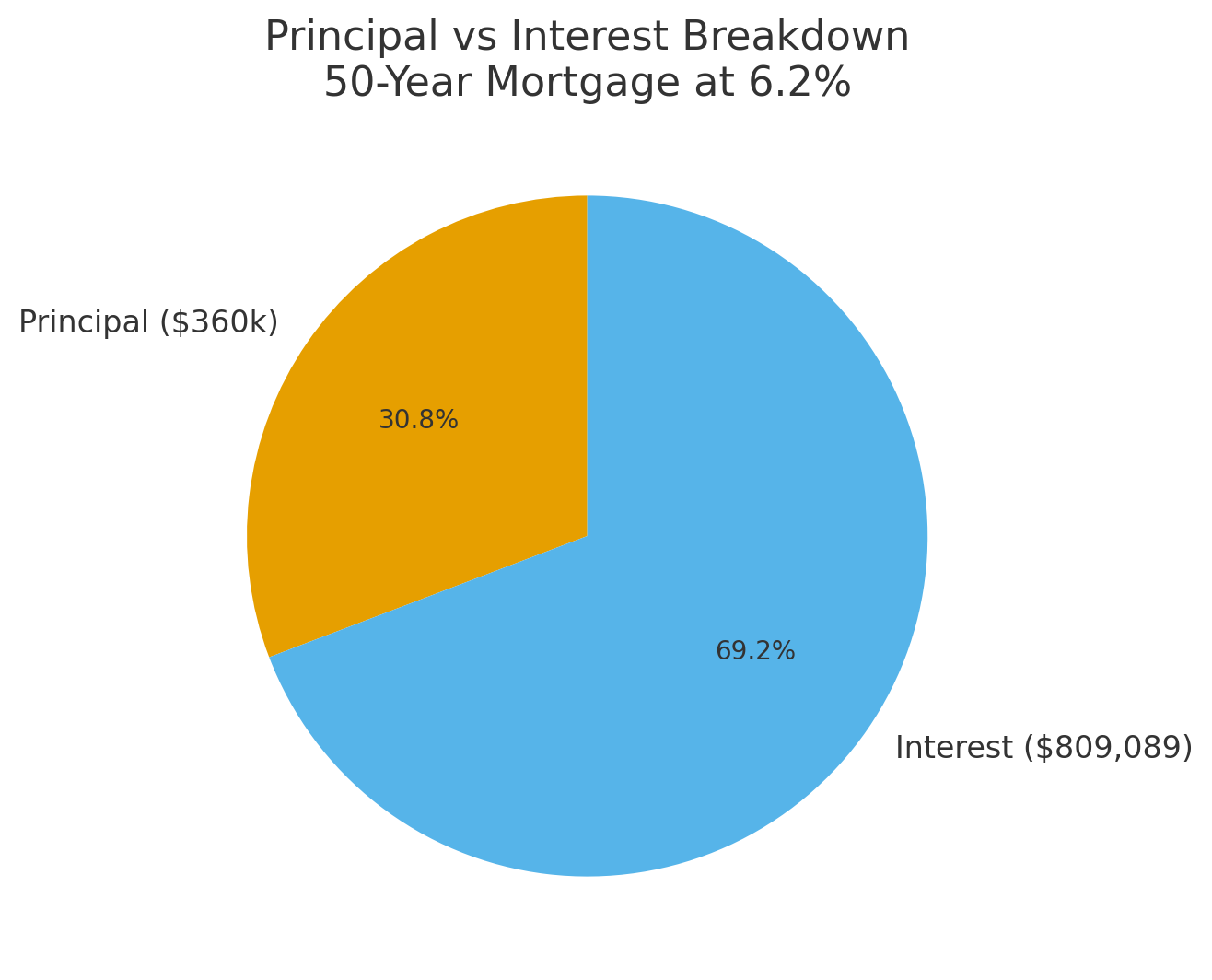

50 Year Mortgage

Oregon Home | Josephine County, Oregon

The 50-Year Mortgage: Pushing the Problem to the Next Generation

How Financing is both a blessing and a curse.

There’s a new idea floating around the housing market: the 50-year mortgage. It’s being marketed as innovation, as if extending a loan will somehow make homes affordable again. But when you run the numbers—and when you pay attention to how people actually live—it becomes clear what’s really happening. A 50-year mortgage doesn’t fix affordability. It stretches the pain across generations—to line the pockets of investment bankers and the subprime loan market.

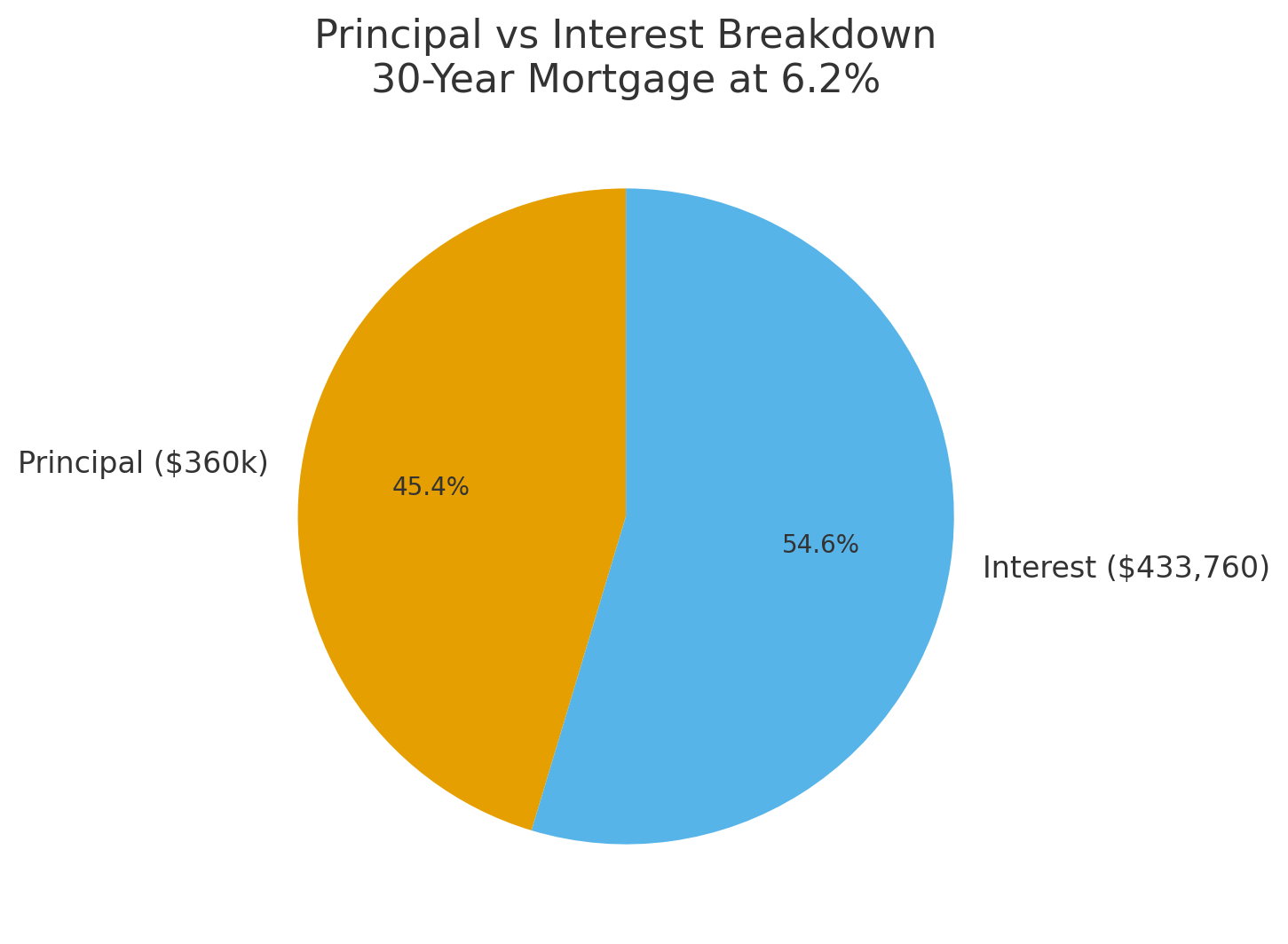

Take a $450,000 home with 20% down. Loan amount: $360,000. To keep this grounded in reality, let’s use a 6.2% interest rate, which matches today’s average mortgage environment.

30 Year Mortgage

The payments drop only about $250 on a 50 year loan, but the total interest nearly doubles—Instead of paying $433,760 dollars, the borrower will now pay an extra $375,000. This wealth is extracted from a working family for the same house. That’s not affordability. That’s wealth being siphoned upward.

And this is where the financial side becomes impossible to ignore. A 50-year mortgage doesn’t just increase the borrower’s cost—it dramatically increases lender profit margins, while the buyer’s payment drops only about twelve percent. It goes from a Monthly payment: ≈ $2,205 to $1,948. On this same loan, the lender earns 87% more interest. That kind of spread in earnings doesn’t exist in any ethical consumer-finance product—it exists in subprime markets built on long-tail, interest-heavy obligations. That’s also assuming the interest rate would be the same, it would actually be more likely to have a higher rate at 50 years than 30.

A 50-year mortgage behaves like an investment vehicle: a predictable, secured stream of payments that can be bundled, sold, and leveraged for decades. It is a dream product for lenders and Wall Street. These loans generate half a century of cash flow that can be packaged into mortgage-backed securities, resold many times, and monetized even more than the 30 year loan.

50 Year Mortgage

And the extraction doesn’t end with the lender. Over a 50-year span, the homeowner will almost certainly pay well over $100,000 in insurance—and in higher-risk markets that sum can climb to $150,000 or more, even $200,000+, quietly adding another layer of extraction. That is a second, hidden wealth transfer almost no one bothers to calculate.

And this part is mathematically unavoidable: no interest rate, down payment, or buy down can change the basic fact that lenders always earn more on a 50-year loan. The structure of amortization guarantees it. The borrower’s monthly savings stay small, but the system’s lifetime revenue grows massively. It’s not hypothetical. It’s mechanical. Longer terms always shift wealth upward.

A 50-year mortgage makes the payment slightly easier today, but dramatically increases the cost over a lifetime. It ensures younger buyers pay into retirement and often leaves children inheriting a property that’s still under debt. When prices outrun incomes, the system doesn’t correct—it adapts. Not by lowering prices or raising wages, but by stretching the timeline of debt far enough that the monthly payment feels tolerable. Meanwhile, the true cost becomes enormous. It’s the quiet inversion of the American dream.

The Land of the People | Douglas County, Oregon

“You will own nothing and be happy” isn’t a slogan if the 50 year mortgage becomes a reality—it’s the natural outcome of a system that treats shelter like an investment vehicle and families like revenue streams. It doesn’t make homes more affordable. It simply stretches the debt far beyond the people paying it. And the next generation is expected to pick up whatever remains. Japan tried this in the 90’s and the market collapsed soon afterward.

For most of human history, societies understood the danger of long-term, unending debt. In ancient civilizations across the Middle East, Europe, and Asia, households crushed under debt didn’t simply struggle financially—many lost their land, their rights, or their freedom. Debt prisons existed because once a family fell behind, escape was nearly impossible. Their time, labor, and future became controlled by the creditor. To prevent this, many cultures instituted structured resets—like the ancient Hebrew practice of releasing debts every seven years. The point wasn’t generosity. It was survival. A society where debt was treated as though it was a crime, is not a free and thriving culture.

For generations, the American home has been the most powerful wealth-building tool ordinary families have—not stocks, not 401k’s or Roth IRAs. The home. It’s the only asset most people will ever own that steadily appreciates while building equity month after month. But a 50-year mortgage quietly breaks that system. The foundation of generational stability—gets pushed so far into the future that many homeowners will never reach it.

The American Dream | Douglas County, Oregon

On a standard mortgage, ownership grows as interest declines, creating a balance where families build wealth while banks earn a return. A 50-year mortgage destroys that balance. The monthly payment barely drops, yet the lifetime interest nearly doubles, transforming the home into a long-term revenue stream for the lender instead of a wealth-building asset for the family living in it.

This is what the American Dream actually looks like — or at least what it used to. Two young people starting a life together. A family able to gather, support, and celebrate their children’s union. A future that feels possible, not mortgaged to death before it even begins. But when you stretch a loan across half a century, you’re not helping young families. You’re not giving them opportunity. You’re taking away the one thing this moment represents: a chance. A chance to own something. A chance to build equity. A chance to start a family without being financially strangled for 50 years. A 50-year mortgage doesn’t preserve moments like this; it quietly erases them. And the next generation deserves better than a dream they’ll never get to dance inside of.

Thank You for Subscribing

Take the leap into rural living. If you have questions about Southern Oregon landscapes, land ownership or country properties, I’d be happy to help guide the way.

Warm Regards,

Dan Amos (Agent of the Wild)